How Does Financing Work for International Buyers?

Unlike domestic buyers, international investors often lack a U.S. credit history or Social Security Number (SSN), which can make traditional mortgage financing seem out of reach. However, specialized loan programs exist to accommodate foreign nationals.

Our Founder, Angela S. Hwang was recently joined by Founder & CEO of HomeAbroad, Amresh Singh, to talk about how financing works for foreign investors, and why the real estate market remains strong in the U.S.

Here’s how it works:

Investment Property Loans

📊 Qualification Based on Rental Income: Lenders assess whether the property’s rental income can cover the mortgage payments.

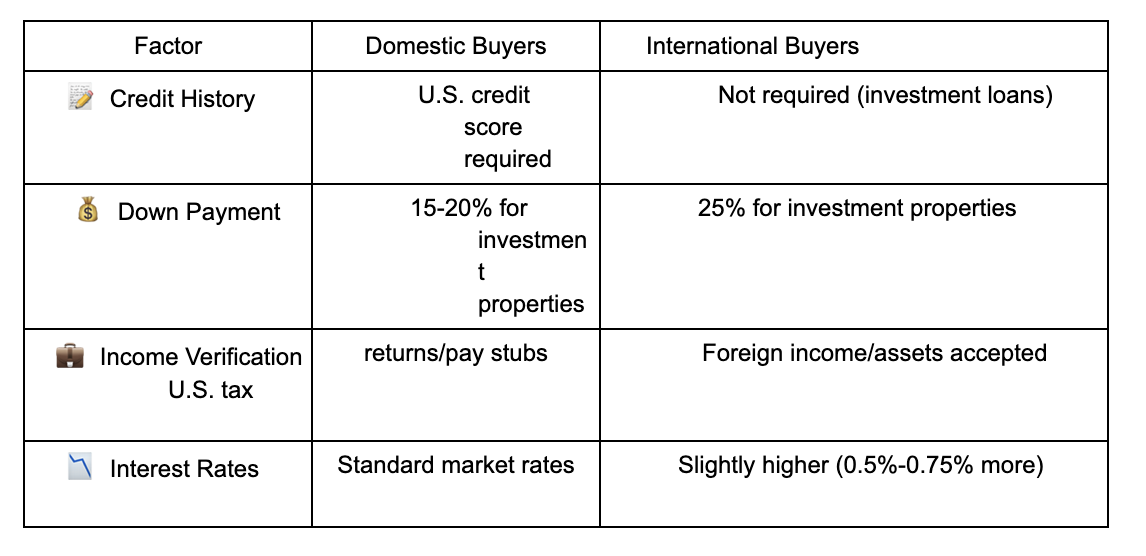

💵 Down Payment: Typically 25% for foreign nationals.

🆔 No U.S. Credit History Required: Instead, the loan is approved based on the property’s cash flow potential.

Second Home Loans

For buyers who plan to use the property part-time (e.g., snowbirds❄). Requires proof of foreign income/assets and an international credit report.

Primary Residence Loans

For those relocating to the U.S., they can use foreign income documentation for qualification.

Key Differences Between Domestic & International Financing

FAQs

"I don’t have a U.S. credit score or SSN. Can I still qualify?"

Yes! Investment property loans rely on rental income, not personal credit.

"Do I need to season my funds for months?"

No. Funds only need to be in your account for 30 days before closing.

"Are interest rates extremely high for foreign buyers?"

No. Rates are only 0.5%-0.75% higher than domestic investor loans—far from hard-money loan rates.

"Can I finance commercial properties?"

Yes, but terms differ. Residential loans are more common due to better leverage and fixed-rate options.

How to Prepare for Your U.S. Real Estate Purchase

Determine Your Investment Goal

Cash flow? Appreciation? A second home? Research markets with strong rental demand

Understand the Costs

Down Payment: 25% for investment properties.

Closing Costs: ~3-4% of the loan amount.

Choose the Right Property

Avoid high HOA fees or rental restrictions.

Use tools like HomeAbroad’s investment property platform to analyze cash flow.

Work with a Specialized Lender

Banks often reject foreign buyers—opt for lenders experienced in international financing.

2025 U.S. Housing Market Outlook

Despite economic fluctuations, U.S. real estate remains a solid long-term investment due to:

Low Inventory: 70% of homeowners have rates below 4.5%, reducing resale supply.

Future Appreciation: If rates drop, demand will surge, boosting property values.

Cash-Out Refinancing: Investors can leverage equity to expand portfolios.

Final Thoughts

International buyers no longer need to pay all-cash for U.S. real estate. With the right financing strategy, you can leverage loans to multiply your investments, generate passive income and benefit from long-term appreciation.

Learn more about how you can get financing to purchase U.S. real estate by visiting HomeAbroad.